How government bonds destroy investment returns

I suspect that most people sense that the dice are stacked against them in the financial system … they are not wrong! Large sections (but not all) of the “asset management” industry appear to be more interested in fee generation than in generating returns for their investors. In fact, those objectives are often diametrically opposed.

Although people groan at the idea of thinking about investments and pensions, this is definitely an area where an ounce of prevention is worth a pound of cure. Spending a few hours now to avoid two common errors could translate into significantly (x2) pension outcomes down the road. One of the mysteries that has bothered me for a very long time is the constant debate over how much government debt to mix in with high return equity in order to generate an “efficient portfolio.”

I suspect that millions … actually, make that billions of manhours have been spent on debating departures from the “classic” 60:40 equity to debt portfolio or a “racier” 70:30 portfolio or a “safer” 50:50 portfolio. This suggests that increasing the amount of government debt in a portfolio make it less risky, yet that same debt yields low returns and is actually quite risky and can generate real (inflation adjusted) losses. In reality, everyone in the know understands that 100% high-return equity is, and always has been, the answer to this question.

Actual returns achieved by Berkshire Hathaway (Warren Buffet CEO) essentially 100% equity 1964 to 2025, from 2025 annual report

How did we end up with these debates?

The first fact that we need to acknowledge is that equity returns over any period of several years are usually significantly higher than returns achieved on debt (Treasury bonds). This is the case nominal or real (i.e.. inflation adjusted) terms.

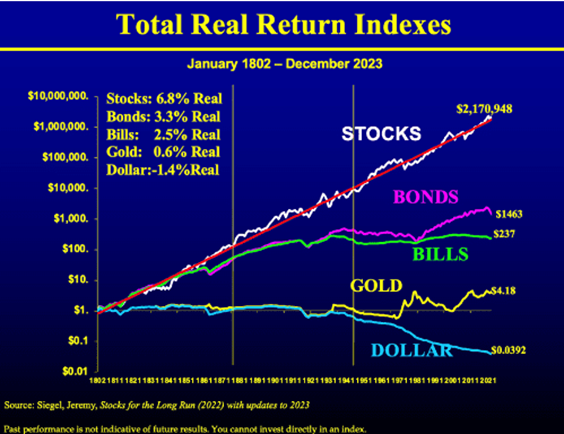

The chart below was included in his book “Stocks for the Long Run” by Professor Jeremy Siegel. It was reproduced in a recent article by WisdomTree Prime (part of the WisdomTree asset management business). I use it because even though the timescale is not perfect for our purposes, it is from a reputable third-party source. The key point is that over a long period of time (222 years) stocks have outperformed bonds by a factor of 1,500 times (2,171.0/1.5).

The question is then if you had USD 10 in 1802 where would you invest it?

Note also the use of a logarithmic scale, that ensures that the other assets such as bonds, bills and gold are visible in this chart – had a regular y-axis scale been used, those other assets would flatline as if glued to the horizontal x-axis.

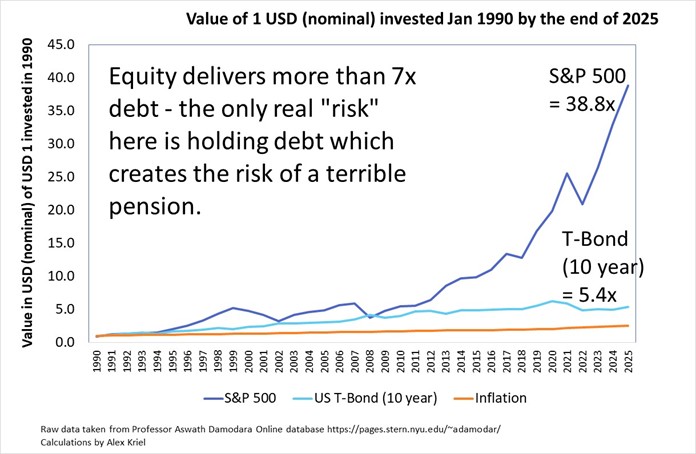

If we zoom in to a period that is likely to be more directly useful to us, say 1990 to 2025, we again see the same staggering out-performance of equity over debt – this data was posted by Professor Damodaran of Stern Business School online.

Note that these returns are historic actual returns and not a theoretical model. Note also that although equity again beats debt by a huge margin, this period includes a period when inflation and interest rates were falling under easy monetary policy, conditions that were very favourable to US Government bonds. This favourable environment reversed in 2022 and bonds began to fall precipitously.

So the next question is: starting in 1990, what assets would you have invested in?

Poor but “efficient”

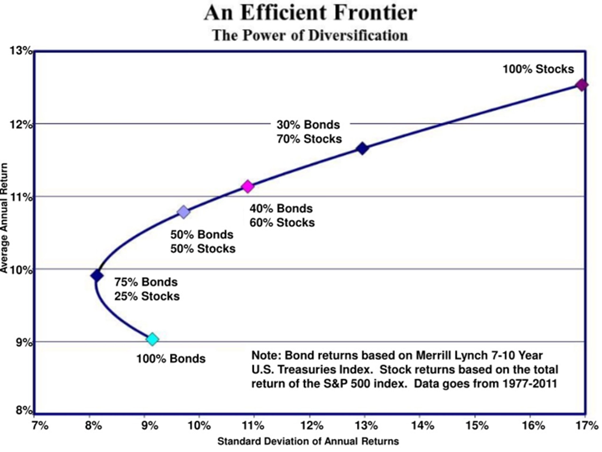

The somewhat preposterous idea that you should dilute equity returns with low-performing debt was hatched in around 1952 by RAND operative Harry Markowitz, when he described an “efficient frontier”. His theory managed to convince people that they should sacrifice asset returns (which determine future pension pay-outs) for volatility (a mathematical measure of how much any particular asset jumps around year on year).

Whereas previously the question asked by those investing pension funds was “How can I maximise returns,” Markowitz reframed it to ask “How much return will I sacrifice in order to minimise standard deviation?” Maximising investment returns while minimising standard deviation was defined as “efficient”. “Efficient” sounds … well, efficient! So much so that seeking the “efficient frontier” became the goal of many investment advisers. In this process, some important things were forgotten: that returns drive actual cash outcomes, that standard deviation is a mathematical construct that can’t be used to fund medical assistance, trips to see overseas grandchildren, or go on a cruise.

I suspect that a private investor would rather have USD 38.80 from a stock index that bounces around rather than USD 5.40 from a bond investment that doesn’t.

Not only are the returns from equity higher, but it also turns out that the basic logic that underpins the “efficient portfolio” theory, namely that shares and bonds tend to move in opposite directions and that combined, they tend to reduce volatility (standard deviation) does not hold over time.

Academia has for the most part been complicit. It is only very recently that a group of academics broke cover and stated the obvious: that (guided by past performance) a portfolio of U.S. and international equity will always beat any portfolio with bonds in it. Specifically, that a portfolio strategy with “no material fixed income allocation” will “dominate[s] conventional stock-bond strategies in building wealth, preserving capital, and generating bequests.”

As a Buffet-type value investor, you are taught that market prices (and volatility) are noise. Mr. Buffet equates the stock market to the eccentric farmer living next door who shouts out prices every day, largely depending on his mood. Ninety-nine times out of a hundred you ignore the eccentric farmer, but if he happens to shout out a high price you sell to him and if a low price, you buy from him. The rest of the time you ignore him.

The interests of the financial institution and the private saver are not the same

Volatility is important for financial institutions which mark their positions to market generally in real time and need to maintain various buffers to handle maximum probable losses, which are in turn calculated by formulae relying on volatility as an input. High volatility creates a headache for the financial institution because it means they have to carry larger buffers to absorb larger potential losses.

But things that are a problem for investment managers are not a problem for a private saver who is aiming to maximise his or her savings in the medium to longer term.

Cui bono?

In addition to supressing the incomes of millions of pensioners, the “efficient frontier” theory (although with other similar theories) also creates a captive audience for low/negative real return government debt in the shape of 40% of every portfolio of every single person who subscribes to the 60:40 convention. Public pension funds in particular have large portfolios of low return government debt and regularly report negligible returns that drag down the weighted average return for the pension fund.

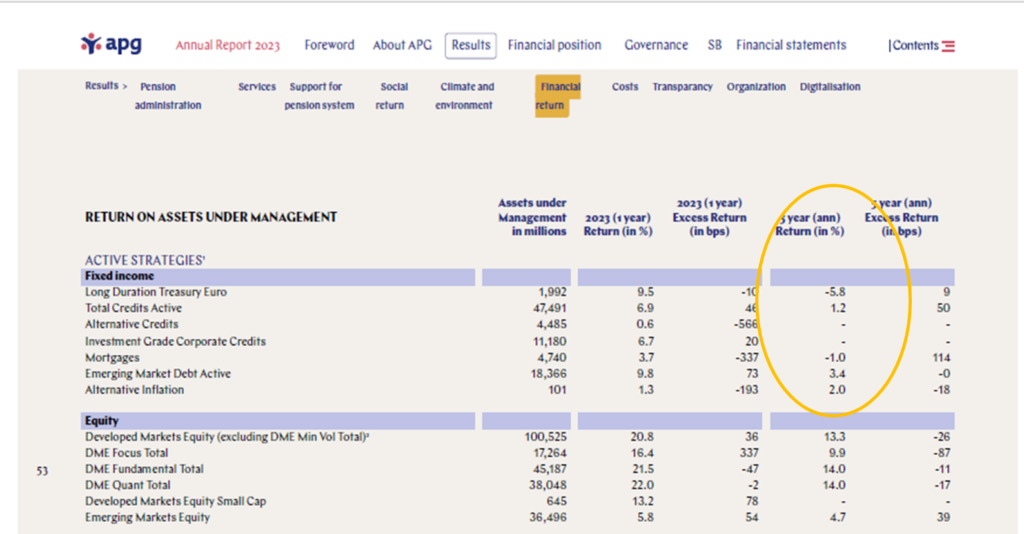

Accounts of large Dutch pension fund manager APG, the obvious conclusion would be to replace the low return fixed income “assets” (circled) with high return equity assets below.

This captive audience will swallow endless amounts of government debt issuance. In the event of debt devaluation through inflation this captive audience (generally the great unwashed) will absorb 100% of the losses. This chicanery is aided by another (related) “truth”, namely the idea that lending to the government (buying T-bonds or gilts) is “risk-free” as in the risk-free rate. In reality, bonds carry risk and they will perform very poorly in an environment of rising inflation. At one point in 2022, the volatility of the largest bond Exchange Traded Fund (“ETF”) was higher than the largest equity ETF.

How we can help

Whatever stage of your pension journey you are at, it is vital that you don’t load up your pension with under-performing “assets” like government debt and high fee/low performance funds. It is also important to have some view of what the world looks like going forward as developed market debt levels explode and government finances deteriorate in an environment of shifting geopolitical power. Sitting down with an advisor to tweak a portfolio from 60:40 to 70:30 isn’t going to cut the mustard and is likely to leave you in a significantly worse position in retirement. Please be aware that we are not investment advisers and do not provide investment advice, but can discuss historic statistics and recent academic papers and opinions that we believe are of interest without giving investment advice.

Caveat

Any discussion is for informational and educational purposes only. It does not constitute investment advice, financial advice, or a recommendation to buy, sell, or hold any securities or investments. The information presented is based on publicly available data and the author’s own analysis as of the date of publication. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. Readers should not rely on any information contained in this article/discussion as the basis for making any investment, financial, or other decisions. You should consult with a qualified financial advisor or conduct your own independent research before making any investment decisions. The author and any affiliated parties expressly disclaim any liability for any loss or damage arising from the use of, or reliance on, the information in this article/discussion.